by Julia Weaver, Managing Director & Family Office Fellow and Chris McGraw, Senior Wealth Strategist

For many business owners considering a sale of their business, maximizing enterprise value becomes a singular focus and the proverbial finish line. Beyond the finish line, however, is the looming reality of the tax haircut this enhanced wealth may face when it passes to heirs. Additional issues around how the family will meet its objectives with the “new” balance sheet must also be considered.

Let’s Start with Taxes

By transferring a portion of their business interest into structures that will avoid gift or estate tax, sellers may retain a greater percentage of the growth in their family’s wealth.

Three-Stage Framework: Pre-and Post-Sale Planning

Stage 1 – Pre-Sale Structuring: Capture Discounts Without Tax Cost

Creating a discounted interest can enhance tax savings. Discounts are typically available for minority non-voting and non-marketable interests, which can generally be created through a fairly simple recapitalization process.

Rather than utilizing $10 million of gift and estate tax exemption to pass $10 million of non-discounted interest, it is better to transfer that same interest at a value that is reduced by a valuation discount, often seen at 30 – 35%. If the business is later sold, the discount evaporates and all shares receive the per-share sale price. In this scenario, nearly $14.3 million of post-sale non-discounted business interest has been transferred (assuming a 30% discount), while utilizing only $10 million of the owner’s exemption. This is referred to as “freezing the discount.”

Stage 2 – Pre-Sale Freeze: Lock In Enterprise Value, Increase Outside the Estate

Future appreciation, or the “pop” in value many business owners enjoy as a result of a successful sales process, may also be structured to occur outside of the taxable estate, further enhancing the retention of family wealth.

Stage 3 – Post-Sale Planning: Prevent Estate Tax on Future Appreciation

After the liquidity event, this newly monetized wealth can remain in tax advantaged vehicles that may continue to protect subsequent growth from estate taxation. Over the future years of wealth accumulation, the potential tax savings can be considerable.

Financial Life After the Business is Monetized

How will the family meet its objectives with the new balance sheet? With the liquidation of what is typically the primary asset of a business owner’s family, the necessity to manage objectives, income and risk becomes paramount. Many families are challenged to successfully navigate the change and sustain wealth across generations. To be prepared, careful financial modeling and testing is needed. The following basic elements of a plan should be considered well in advance of the sale of the business:

-

- Define objectives with realistic values and growth expectations taken into consideration.

- Determine the appropriate size of a safety net for the family.

- Design a strategy to support and continue the family’s lifestyle.

- Identify aspirational objectives and generational intentions.

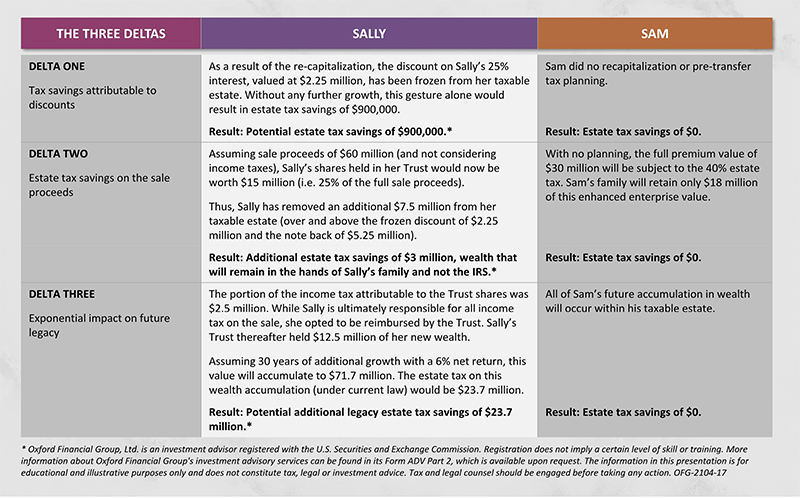

Tax Impact Analysis: A Tale of Two Sellers

We assume two sellers in a highly fictional “exact” situation, but for the fact that Seller One (Sally) was referred by her investment banker to her wealth planning team for pre-transfer planning. Seller Two (Sam) was not. Both businesses were originally valued at $30 million (the “base” value). They each concluded a very successful sales process and sold their businesses in three years for $60 million. After taxes and costs of $10 million, the net proceeds from each sale was $50 million. However, both sellers are subject to federal estate tax. In other words, without any planning, when Sam transfers wealth to his or her heirs, the IRS becomes the recipient of 40% of this appreciation in enterprise value resulting from the successful sales process.

Sally’s Planning Strategy

- Three years prior to the sale, Sally implemented a strategy to remove a 25% minority, non-voting interest from her taxable estate, retaining full control of the business’

- Sally recapitalized her interest into voting and non-voting shares.

- Sally then created a trust that is excluded from estate (but not income) taxation, known as an Intentionally Defective Grantor Trust, or “IDGT,” referred to herein simply as her “Trust.”

- Sally seed funded her Trust with a relatively small gift.

- Sally then sold a 25% non-voting interest to her Trust, which qualified for a 30% discount, and thus post-discount was valued at $5.25 million.

- Sally took back a 9-year, $5.25 million, interest-only balloon note, with a required mid-term AFR.

- The sale to Sally’s Trust avoided capital gains due to its structure as a Grantor trust and the proper crafting of the terms of the sale.ii

- Capital gains will, however, be recognized upon the sale of the interest to a third party, including on all shares held in Sally’s Trust.

The examples presented are hypothetical in nature and are not guaranteed outcomes. They are provided for illustrative purposes only. Projected results are based upon the assumptions as presented, which may differ materially from any actual events or conditions.

Unique Times / Unique Situations

As with all elements of planning, pre-transfer planning should be done in coordination with the business owner’s comprehensive estate plan. When appropriate to meet the core goals and objectives of the business owner, pre-transfer planning can have a significant impact on the family’s enduring wealth. Your Oxford team of advisors can assist in determining the proper strategy for your unique situation.

iSally’s advisors crunched the numbers and selected a recapitalization of Sally’s interest into voting and non-voting shares. After properly capitalizing a trust that is excluded from estate taxation (known as an Intentionally Defective Grantor Trust, or “IDGT”), Sally sold a 25% discounted minority interest to the IDGT in return for a 9-year, $5.25 million interest-only balloon note (the amount of the originally discounted value of her interest), with a required mid-term AFR. This “sale” avoided triggering any capital gain due to the properly crafted structure of the sale and terms of the IDGT.

iiThe sale to Sally’s Trust is only successful when the appreciation in the underlying asset exceeds the AFR hurdle rate.

Oxford Financial Group, Ltd. (“Oxford”) is a Registered Investment Advisor (“RIA”) with the U.S. Securities and Exchange Commission (“SEC”) and is headquartered in Carmel, Indiana. Registration with the SEC does not imply a certain level of skill or training. Additional information about Oxford, including our Form ADV and Privacy Policy, is available upon request by calling 800.722.2289 or emailing info@ofgltd.com. The content of this presentation is intended for educational and illustrative purposes only. It should not be construed as investment, tax, or legal advice, nor as a recommendation or offer to buy or sell any security or investment product. Tax and legal counsel should be engaged before taking any action. This material has been prepared using original sources believed to be reliable, but no representation is made as to its accuracy or completeness. The views expressed are those of Oxford as of the date of the presentation and are subject to change based on market, regulatory or economic conditions, which may not occur as anticipated. For full disclosures and disclaimers, please visit https://ofgltd.com/home/disclaimers. OFG-2604-11